The Headline Number And The Household Experience

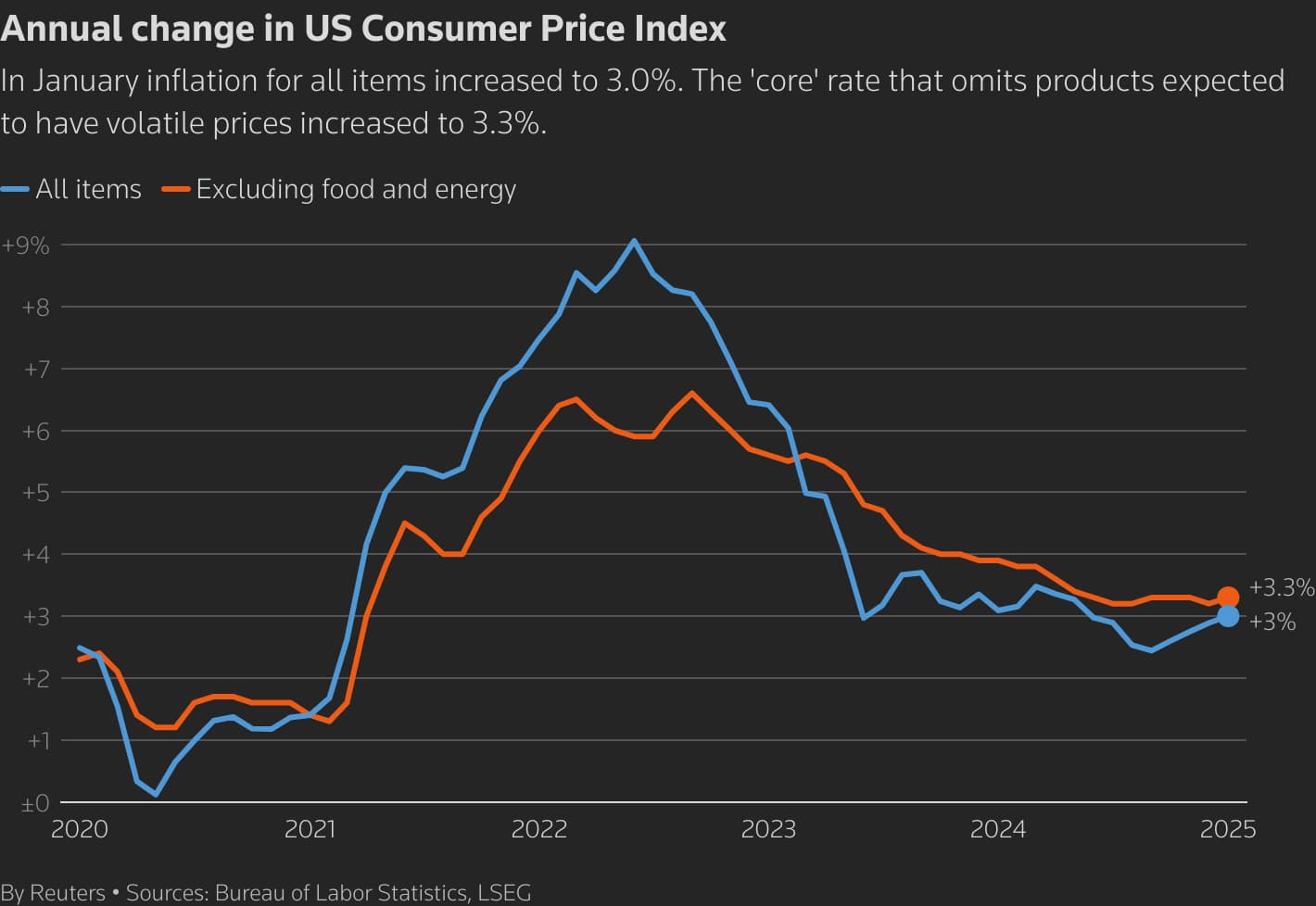

The headline Consumer Price Index print for March 2026 came in at 3.2 percent year over year, with core CPI at 3.4 percent and shelter inflation at 4.7 percent. The numbers are, in their own terms, accurate. The numbers are also, when applied to the consumption basket of the U.S. middle class, materially understated. To put it plainly, the inflation the middle class is experiencing exceeds the inflation the headline number is measuring, and the gap is the gap that explains the disconnect between the macroeconomic narrative and the household frustration that polling has documented for three consecutive years.

The arithmetic is straightforward. The CPI basket weights consumption categories by the average household's spending pattern. The average is calculated across the full population. The middle class, defined here as households earning between approximately $60,000 and $120,000 in annual income, consumes a basket whose category weights diverge from the population average in three specific ways. The divergence in each category is in the direction that has experienced higher inflation than the headline number suggests.

The Three Categories That Are Off

The first category is housing. The CPI shelter component is built around owners' equivalent rent and rental price surveys. The shelter component runs at 4.7 percent year over year. The middle-class household, particularly the household at the marginal home purchase decision, experiences housing inflation at the rate of the median home price change, which ran at 7.8 percent year over year in March, and at the rate of the median mortgage payment, which ran at materially higher rates due to the rate path on the underlying financing. The middle-class household experience of housing inflation is closer to 9 percent than to 4.7 percent.

The second category is durable goods that the middle-class household replaces on a four to seven year cycle. Vehicles, appliances, and furniture all show CPI inflation in the low single digits because the CPI measures the rolling average of all purchases in those categories. The middle-class household making the replacement purchase in the current cycle experiences the price level at the current quality-adjusted point in the cycle, which has, for vehicles in particular, run materially above the CPI rate. The replacement-cycle household experience is closer to 12 percent than to the CPI rate.

The third category is the basket of services the middle-class household consumes at higher intensity than the population average. The categories include child care, after-school programs, summer camps, orthodontia, sports equipment and league fees, and the discretionary services associated with raising school-age children. These categories show inflation rates in the high single digits to low double digits across the trailing year. The CPI weights them at the population average, which understates their weight in the middle-class basket considerably.

The Aggregate Mismatch

The aggregate mismatch, when one weights the actual middle-class consumption basket using the underlying category-level inflation rates, comes out to a household inflation rate of approximately 5.6 to 6.2 percent year over year, against the headline 3.2 percent print. The mismatch is large. The mismatch is also persistent, which is the part that matters for household perception. A 5.6 to 6.2 percent inflation rate, sustained across three years, compounds to a cumulative household price level increase of approximately 18 to 19 percent. The household is, in fact, paying that much more for the same basket.

The data are unambiguous. The Bureau of Labor Statistics publishes the underlying category-level inflation rates with sufficient granularity to permit the recalculation. The Federal Reserve Bank of St. Louis has, in research notes over the trailing eighteen months, acknowledged the divergence between the headline measure and the income-band-specific household experience. The acknowledgment has not, however, produced a corresponding shift in the way the Federal Reserve's policy committee discusses inflation in its public communication.

The Political Implications

The political implications follow from the household experience rather than from the headline. The polling that has documented voter frustration with the economy for three consecutive years has, in the same period, registered headline inflation prints that the macroeconomic commentary has described as low or moderate. The gap between the household experience and the commentary is the gap that drives the polling result. The voters are not, as the commentary has occasionally suggested, mistaken about their own household economics. The voters are accurate about their own household economics. The commentary is, by the basket it is using, mistaken.

One might observe that the commentary's error is convenient for the political coalition that prefers the headline framing. The observation does not require the assumption of bad faith. The commentary's reliance on the headline measure is the natural posture of an economic policy class trained on the macroeconomic frame. The frame is, however, the wrong frame for understanding the household-level political effect. The wrong frame produces the wrong forecast. The wrong forecast produces, in the political domain, the surprise the commentary class registers when the household-level voters cast the votes they have been signaling they would cast.

What The Federal Reserve Is Watching

The Federal Reserve is, in its working-level analysis, watching the divergence between the headline measure and the household-specific experience. The working-level analysis has not, however, produced a change in the Committee's articulated framework, which continues to treat the headline measure as the operational benchmark for policy decisions. The Committee's institutional caution about modifying the framework is rational at the institutional level. The caution is also, at the household level, the caution that produces the persistent gap between Federal Reserve commentary and household experience.

The Committee's room to ease policy, even modestly, depends on whether the household-experienced inflation rate moves down materially. The household-experienced rate has not moved down. The Committee, given the framework it operates under, will continue to treat the headline rate as the operative measure. The household will, in the meantime, continue to live the experience that the macroeconomic commentary does not adequately characterize.

The Forward Read

The forward read is that the household-experienced inflation rate will, on the available data, continue to run materially above the headline rate through at least the back half of 2026. The political consequences will continue to register at the polling level. The Federal Reserve's framework will continue to use the headline measure. The gap will continue to be the gap that explains why the political class and the household class are reading from two different sets of numbers.

To put it plainly, the household is correct about its own arithmetic. The arithmetic is the arithmetic the political class will eventually have to engage with on its merits. The market has a way of correcting political fantasy. The household, on its own arithmetic, has been doing the correction in real time. The correction is the data.