The Consolidation Data

The Federal Trade Commission publishes hospital consolidation data through its merger review process. The data show that approximately 1,640 hospital mergers and acquisitions have closed over the trailing fifteen years. The volume of activity is high. The geographic concentration of the activity is higher than the aggregate volume suggests. Approximately 380 metropolitan statistical areas have seen at least one significant consolidation event in the trailing decade. Of those, approximately 220 have seen the local hospital market move from a multi-system competitive structure to a one-system or two-system dominant structure.

I see this every day in my clinic. The clinic I run sits in a regional market where the dominant health system has, over the trailing eight years, acquired three of the four other hospital operators in the regional service area. The fourth operator was the smallest at the start of the consolidation cycle and remains the smallest now. The dominant system controls, by the most recent market analysis I have access to, approximately 78 percent of the regional inpatient market and approximately 62 percent of the outpatient market. The consolidation has produced the kind of pricing power that the market structure suggests.

The Price Effect

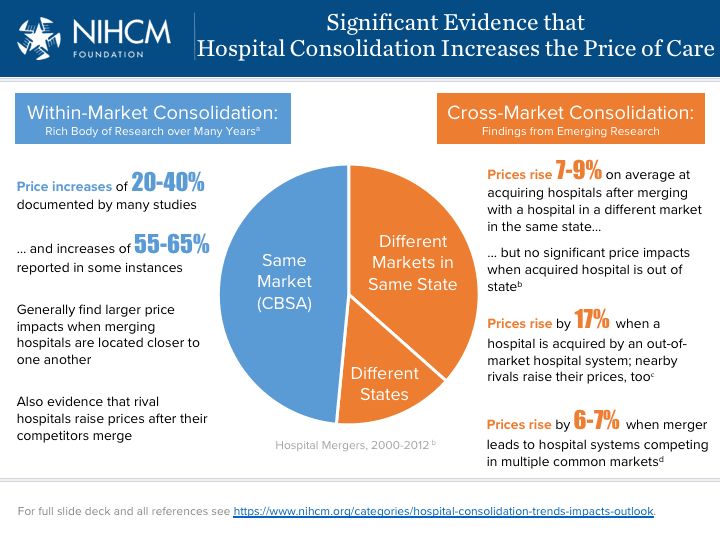

The price effect of the consolidation is documented in the academic literature with consistency that the policy debate has not adequately engaged with. The two leading studies, both published in 2024 and updated in 2025, examined price effects in approximately 90 consolidation events using regression methodologies that control for the relevant non-consolidation variables. The studies found average price increases of 12 to 18 percent across the consolidating systems' patient populations within three years of consolidation closure. The price increases were larger in markets with higher post-consolidation concentration and smaller in markets with lower concentration.

The price increases compound at the individual procedure level. The same diagnostic imaging study, performed in a market where the dominant hospital system charges the median post-consolidation rate, costs approximately 38 percent more than the same study performed in a market without significant consolidation. The same outpatient surgical procedure, performed in a high-concentration market, costs approximately 24 percent more than in a low-concentration market. The numbers are not subtle. The numbers explain a substantial portion of the healthcare price inflation that has consistently outpaced general inflation across the trailing two decades.

The FTC's Posture

The Federal Trade Commission's posture on hospital consolidation has been, across the trailing two decades, a posture of selective enforcement against the largest and most clearly anticompetitive transactions. The selectivity is the result of resource constraints and of the analytical complexity that hospital market analysis involves. The selectivity has, by the consolidation data, produced an enforcement posture that has not constrained the underlying consolidation trend.

The FTC's recent actions, including a renewed merger review framework published in 2024 and several high-profile enforcement actions over the trailing two years, have signaled a more aggressive posture. The signaled posture has not yet translated into a measurable reduction in the consolidation rate. The signal may, in time, produce the reduction. The signal has not yet done so.

The Regulatory Side

The regulatory side of the consolidation story is the side that produces some of the most important effects on smaller practices like mine. The post-consolidation environment includes regulatory frameworks at the federal and state level that have, over the trailing decade, been shaped in directions that advantage large hospital systems relative to independent practices. The advantages include reimbursement architecture, certificate-of-need processes in the states that have them, and the various pay-for-performance frameworks that the Centers for Medicare and Medicaid Services have rolled out.

None of the regulatory frameworks was designed, in principle, to advantage large systems over independent practices. Each of them, in practice, has produced advantages for large systems because the large systems have the administrative infrastructure to comply with the framework's requirements more cost-effectively than the independent practice does. The cost-effective compliance is the operational advantage that, over time, compounds into the market-structure outcome the consolidation data documents.

What This Means For Patients

What this means for patients is straightforward and is the part the policy debate is most reluctant to engage with on its merits. Patients in high-concentration hospital markets pay materially more for the same services than patients in low-concentration markets. The price differential is, in many cases, larger than the differential between patients with insurance and patients without insurance. The differential is not adequately characterized in any of the consumer-facing healthcare price reporting tools the federal government and the state governments have promoted.

The patient has, in the high-concentration market, limited practical recourse. The patient cannot, in most cases, travel to a low-concentration market for routine care. The patient cannot, in most cases, negotiate the post-consolidation prices the dominant system charges. The patient can, in some cases, choose a non-dominant provider when one exists, but the choice is constrained by the network arrangements the patient's insurance carrier has negotiated, which themselves reflect the same consolidation dynamics the patient is trying to avoid.

The Forward Read

The forward read on hospital consolidation is that the trend will continue absent material changes in the enforcement and regulatory frameworks. The FTC's more aggressive posture may slow the trend at the largest transactions, but the trend's principal driver is the mid-size transactions that, individually, do not trigger the largest enforcement attention. The mid-size transactions, in aggregate, produce the market-structure outcomes that the price data document.

In practice, the policy response that would actually constrain the consolidation trend would require both enforcement-side action and regulatory-side action, sustained across multiple administrations. The political conditions for that kind of sustained action are not currently visible. The patients will, in the meantime, continue to pay the prices the consolidated markets produce. The independent practices will, in the meantime, continue to absorb the regulatory cost differential that the consolidated systems do not absorb. The market structure is what it is. Washington has never changed a bedpan, and Washington has not, in twenty years, changed the consolidation trajectory that has, in slow motion, restructured the U.S. healthcare market.